This is one of the most common questions we receive from foreign owners of U.S. entities.

Short Answer:

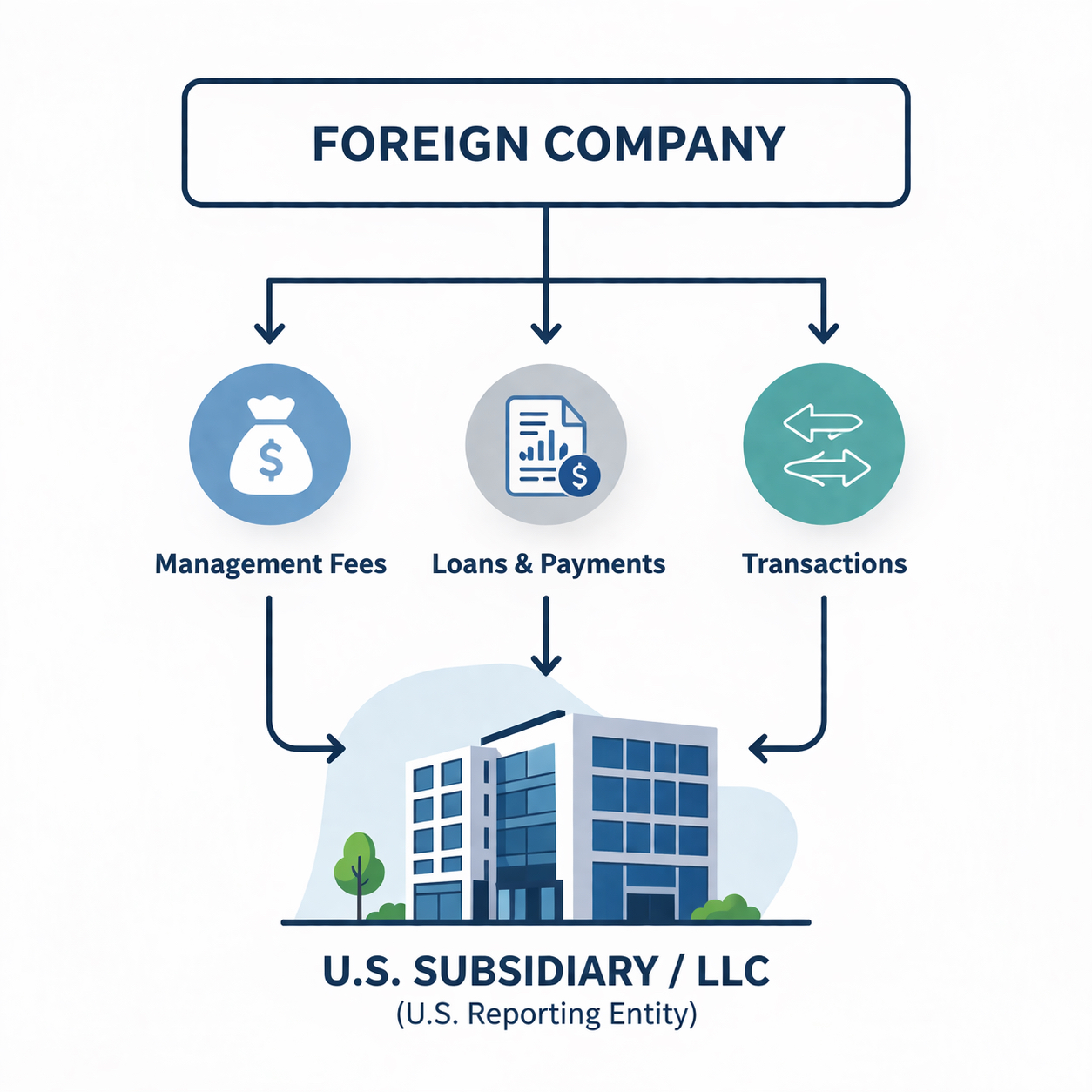

You need to file Form 5472 if a U.S. reporting corporation or a foreign corporation engaged in a U.S. trade or business has reportable transactions with a related party.

Explanation:

Form 5472 applies to three common situations. First, a U.S. corporation that is at least 25 percent foreign owned must report transactions with related foreign parties. Second, a foreign corporation engaged in a U.S. trade or business must report certain transactions with related parties. Third, a foreign-owned U.S. disregarded entity is treated as a reporting corporation for these purposes.

In the case of a foreign-owned U.S. LLC, the entity is required to file Form 5472 along with a pro forma Form 1120, even if it is otherwise disregarded for tax purposes.

Example:

A foreign parent owns a U.S. subsidiary that pays management fees to the parent. These payments must be reported on Form 5472.

Separately, a foreign individual owns 100 percent of a U.S. LLC and contributes funds to the entity. That contribution may also be treated as a reportable transaction.

Common Mistake:

Failing to distinguish between a U.S. subsidiary, a U.S. branch of a foreign corporation, and a foreign-owned disregarded LLC.

When to Get Help:

Form 5472 carries significant penalties if not filed correctly. We would be happy to review your structure and confirm your filing requirements.

If this situation applies to you, we would be happy to review your structure and confirm your filing requirements.